April 2026

Introduction

President Trump has said America is ‘finishing the job’ in Iran. But Iran and other regional actors, rather than Trump alone, are likely to determine when and if that can be achieved

The conflict in the Persian Gulf has now entered its second month. In recent weeks the impact has moved from short term market volatility to more persistent and wide-ranging economic effects across the world. President Trump is widely known as a keen follower of markets, and the health of the US economy and financial markets is likely to be something he has been paying close attention to, especially with the US mid-term elections approaching later this year.

Many believe he will look to strike a deal and declare victory before any lasting economic damage is inflicted on the US people and markets. However, even if there is de-escalation in the conflict, the issue now is how long the disruption lasts and how it impacts different industries and countries, including the UK.

Initial Market Reaction

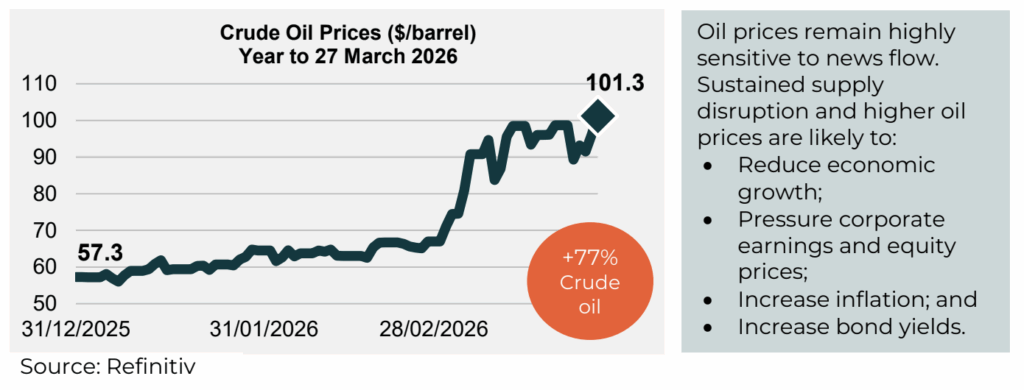

The immediate impact of the conflict was clearly seen in oil and energy markets. Around 20% of the world’s oil production flows through the Strait of Hormuz, which has effectively been closed since the conflict started. The impact could be summarised as follows:

More recent and less visible impacts

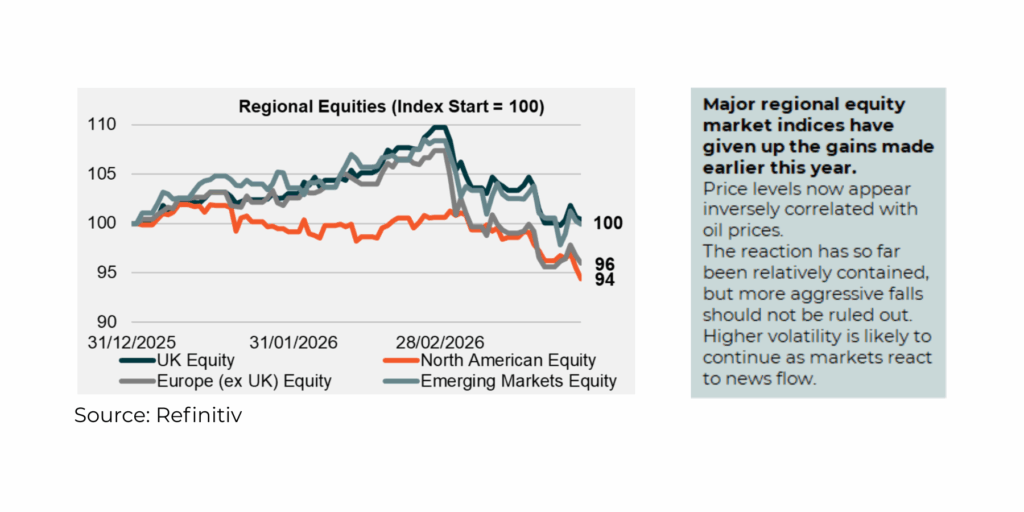

From a markets view, what started as a short-term bout of volatility is increasingly spreading wider and becoming more entrenched. Even if there is a ceasefire, trade and oil will take time to return to some sort of normality in the region, with shipping companies and insurers remaining cautious about the risks in the area.

The Houthis entering the fighting may initially sound like additional noise in an already busy scenario. However, it significantly complicates matters and potentially delays the region returning to normality: in a similar way to Iran and the Strait of Hormuz, they have the ability to restrict movement through the Red Sea and therefore the Suez Canal. A similar pattern took place during the Gaza conflict, and even after a ceasefire by the Houthis in May 2025, it took months for shipping volumes to recover meaningfully. This reflects the lag between any immediate reduction in threat and trade flows normalising.

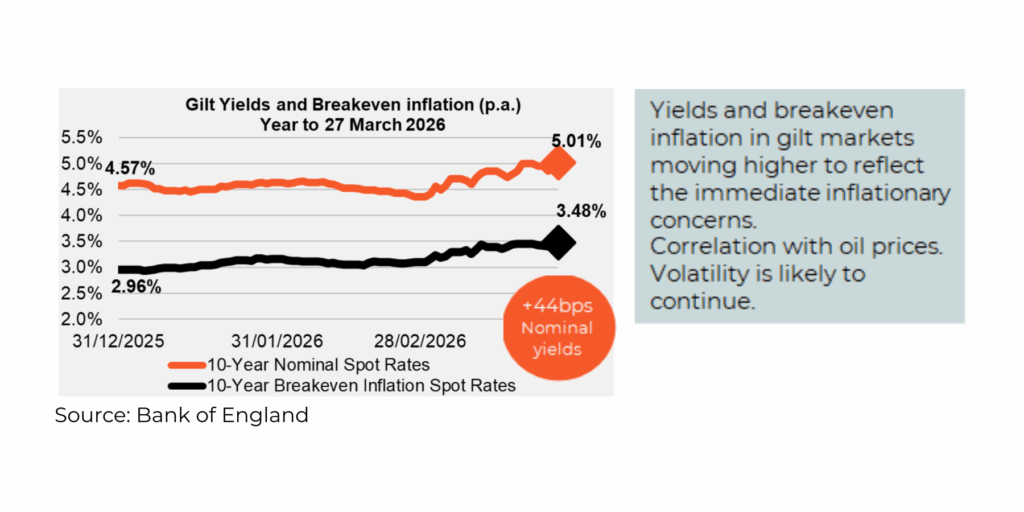

The impact is not just on oil and natural gas. If disruption continues, the higher cost of energy will impact the price of goods and energy-intensive products such as fertilisers, which will in turn impact food inflation. This is also likely to impact economic growth in the region, Asia and beyond, leading to weaker corporate earnings. Markets are increasingly focused on the ongoing constraints the conflict imposes on energy, supply chains, policy decisions and their impact on inflation and growth.

How does that translate in practice? Governments may need to intervene with pre-emptive policies in their economies. This has already happened with South Korea announcing fuel price caps and Australia and India already reducing fuel taxes. Reduced working days, subsidised public transport and curbs on fuel consumption are now on the rise. Central banks may then need to tighten monetary policy in the medium term, which matters for government bond yields and liability hedging, especially inflation volatility. The chain of events has now evolved as follows:

What happens next: two scenarios

A common view is that Donald Trump will seek to avert excessive and lasting economic damage, not least because of the impacts on markets and the upcoming US mid-term elections later this year.

The market reaction and durability of any recovery will depend on whether the resolution is real and lasting, or simply a pause. Damaged energy infrastructure will take time to restart, and disruption to transport may persist for weeks or even months after fighting stops. We have highlighted two possible scenarios here, with a third (further escalation) also a possibility.

Managed de-escalation (most optimistic)

- President Trump applies sufficient pressure on all parties and a ceasefire holds.

- Oil prices fall back, equity markets recover, gilt yields stabilise.

- Inflationary pressures ease, though not immediately back to pre-conflict levels and supplies are slow to recover.

- Markets remain volatile as the durability of any deal is tested.

Prolonged disruption (looking more likely)

- Trump signals de-escalation but Iran or regional proxies do not stand down.

- Markets price in relief prematurely, then reprice sharply.

- Prolonged closure of the Strait feeds into sticky inflation in multiple regions and sectors.

- Tension emerges between fiscal loosening and tightening monetary policy.

- Equities and growth assets face a more severe, more lasting correction.

The key variable is whether the parties required to sustain any agreement to keep the peace are willing or able to deliver it. We believe that is the question to watch over the coming days.

What should trustees and investors do now?

Market dislocations and geopolitical risks are nothing new to long term investors and knee-jerk reactions are rarely useful in periods of geopolitical induced volatility. The priority now is monitoring, not making reactive asset allocation changes and here is a framework to help decision-making:

| Investor type | Action |

| DB Pension trustees | Check collateral waterfall resilience: LDI funds are much more resilient than before the 2022 gilts crisis, but rising yields may trigger LDI de-leveraging calls. Review cashflow strategy to ensure the scheme has sufficient liquidity without relying on selling assets at depressed prices. Monitor inflation hedge ratios regularly. Sharp moves in breakeven inflation can quickly shift these. Credit spreads have been steadily increasing from their historic lows and gilt yields have increased. This could create opportunities to move (back) into credit or increase hedging if appropriate. Consider wider integrated risk management, such as impact on employer covenant. For schemes which don’t currently have this, consider ongoing regular (e.g. quarterly) funding level monitoring, which can highlight issues to address. |

| DC Pension trustees | Review asset exposures, including equity composition where appropriate. Member communications if market moves accelerate, to reassure and mitigate potential switching risk by members. Impact on private market allocations: delays in valuations may mask underlying volatility in prices. |

Further updates

We will publish a further update if and when events unfold and there are material developments.

However, please contact us if there is anything that you would like to discuss in the meantime.