We have been tracking the changes in DB transfer value redress since 2018. Whilst the change in the latest quarter has been modest, this is far less true for the period as a whole. So, we have taken the opportunity to revisit the key themes over the last few years.

Our Approach to Tracking

For simplicity, we track what the level of redress would be for a typical consumer seeking redress and how this would change over time. One addition we have introduced today is to reflect that the level of redress payable will, in addition to reflecting current market conditions, depend on:

- The generosity of the original transfer value: The amount of redress owed is directly influenced by the generosity of the original transfer value. Larger transfer values typically result in lower potential redress, assuming other factors remain constant.

- Investment performance since the transfer: The performance of investments made with the transferred funds also plays a critical role. Strong investment performance can reduce the need for redress, as the individual may have achieved returns that offset any potential loss from leaving the DB scheme.

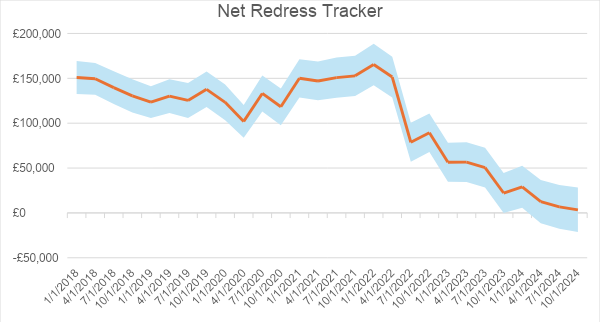

The result is that we show a range of outcomes dependent on the generosity of the original transfer value and investment performance since the transfer.

While the absolute values on the chart below are interesting, it is the movement over the period on which we focus.

The Impact of Rising Gilt Yields

One of the primary drivers in the level of redress payable is gilt yields. Gilts, or UK government bonds, are a crucial component in calculating the redress owed to individuals who have transferred out of DB schemes. When gilt yields rise, the present value of future pension liabilities decreases, leading to lower redress amounts. This is because the higher yields imply a higher discount rate, reducing the lump sum needed today to meet future pension payments.

The Redress Tracker data shows significant falls in redress values over the years. Here are some key observations:

- Initial High Values: In the earlier period (around 2018 – 2021), redress values were relatively high reflecting the period of lower gilt yields.

- Steep decline: Through 2022, as gilt yields began to rise steeply, there was a noticeable decline in redress values.

- More recently: The rate of decline in redress has slowed with it effectively flattening over the last two quarters.

What Does This All Mean?

As is suggested by the chart, we are seeing many instances where no redress is payable at the moment. These will tend to be those consumers who transferred from pension schemes paying generous transfer values – those that had moved into very low risk investment strategies which led to higher transfer values. But there remain many cases which still result in a loss and redress being paid.

For consumers this can be confusing; expecting redress but receiving none. And for IFAs, this makes planning very difficult especially with the potential requirements of CP23/24 coming down the line.

If you need help with your redress calculation, get in touch with us.

Broadstone – redress specialists for over 30 years. For more information – visit us here.

Brian Nimmo – [email protected]

Simon Robinson – [email protected]

")